New CPF & Loan Rules

w.e.f 10 may 2019

Purpose: For more flexibility to buy a home for life while safeguarding retirement adequacy.

Reason: New rule takes into account the changing needs and higher life expectancy of Singaporeans.

Reason: New rule takes into account the changing needs and higher life expectancy of Singaporeans.

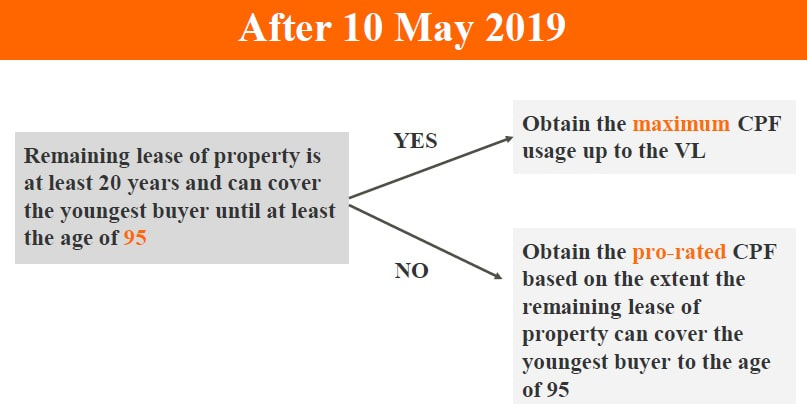

New rule's effect on your CPF:

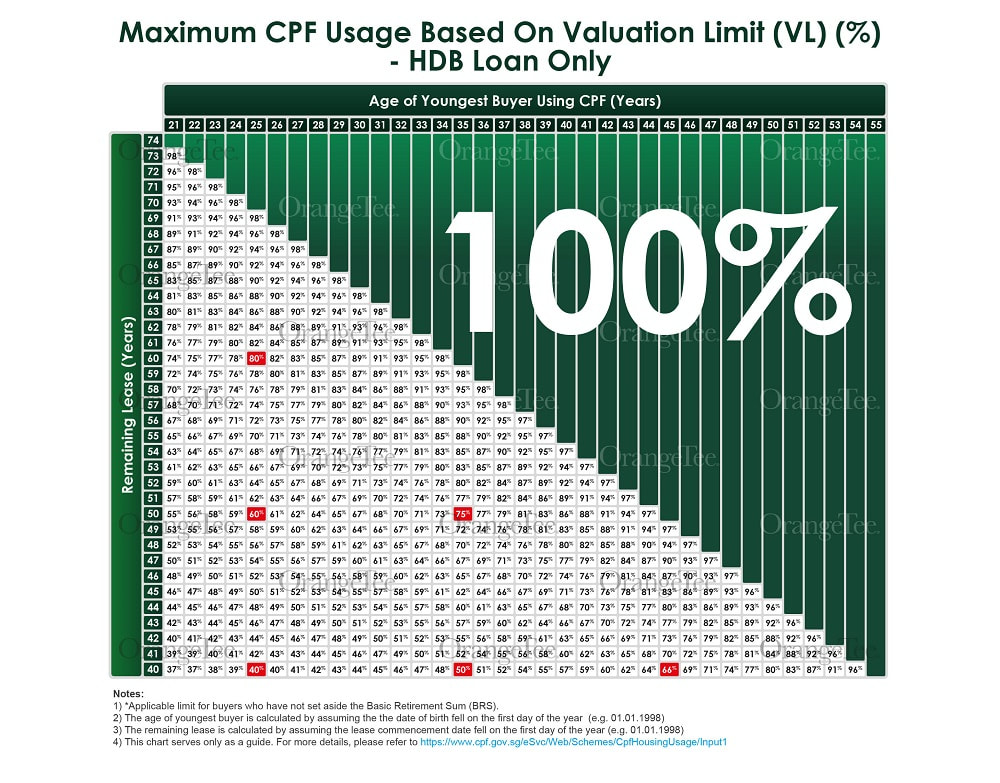

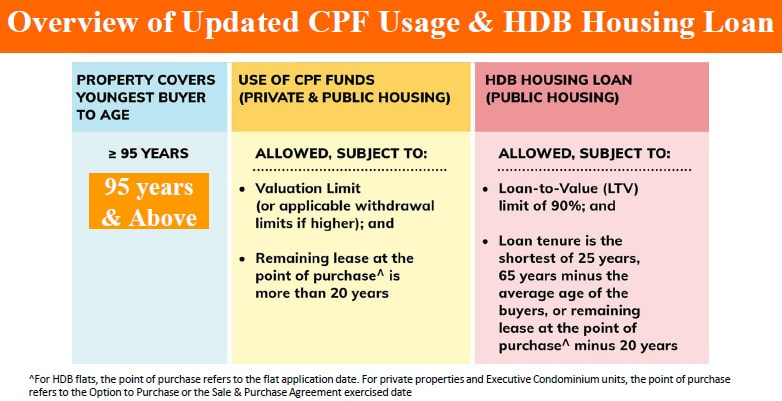

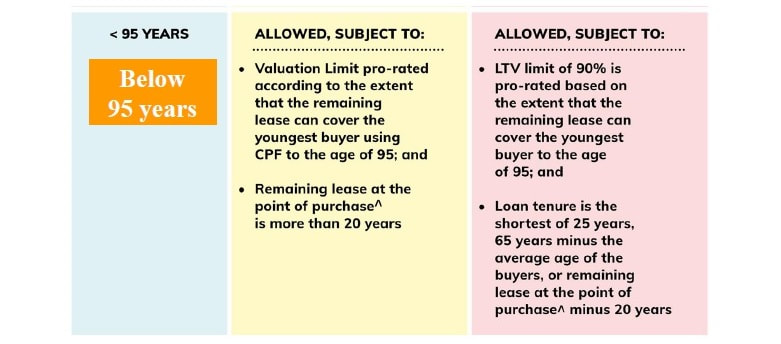

How much your CPF can be used for property purchase will depend on the extent the remaining lease of the property can cover the youngest buyer to the age of 95

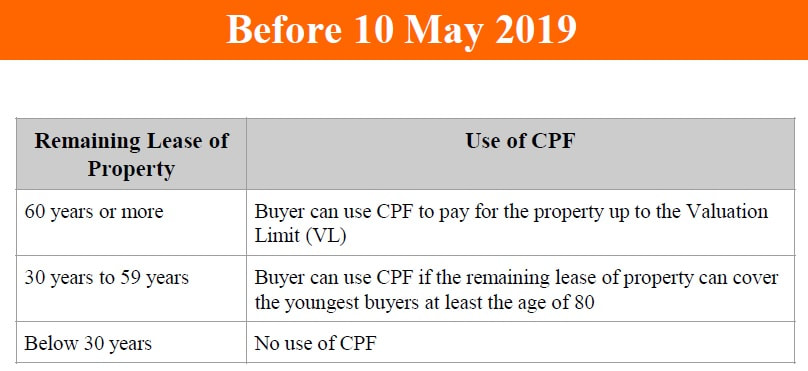

Old CPF Rules

|

New CPF Rules

|

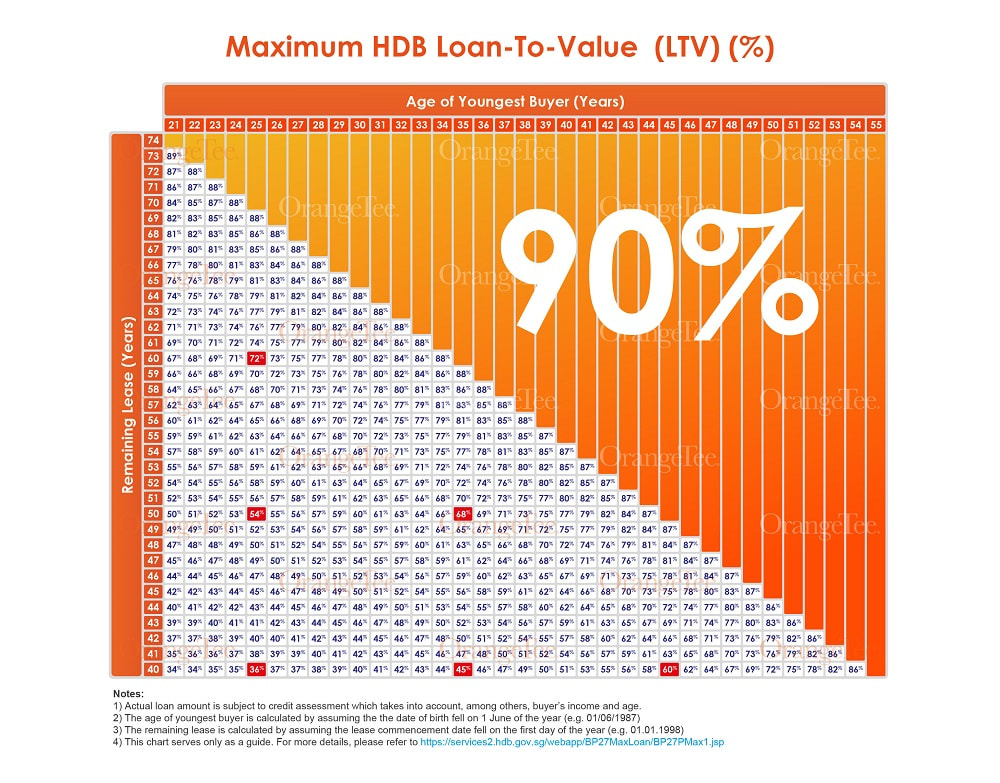

Previously, buyers of HDB flats faced restrictions on the amount of HDB housing loan they could get to purchase flats with remaining leases of less than 60 years.

With this update, buyers will now be able to take a HDB housing loan of up to the full 90% Loan-to-Value (LTV) limit, if the remaining lease of the flat can cover the youngest buyer to the age of 95.

If the remaining lease of the flat cannot cover the youngest buyer to the age of 95, they can still take an HDB loan but the LTV limit will be pro-rated from 90%, based on the extent that the remaining lease can cover the youngest buyer to the age of 95.

With this update, buyers will now be able to take a HDB housing loan of up to the full 90% Loan-to-Value (LTV) limit, if the remaining lease of the flat can cover the youngest buyer to the age of 95.

If the remaining lease of the flat cannot cover the youngest buyer to the age of 95, they can still take an HDB loan but the LTV limit will be pro-rated from 90%, based on the extent that the remaining lease can cover the youngest buyer to the age of 95.

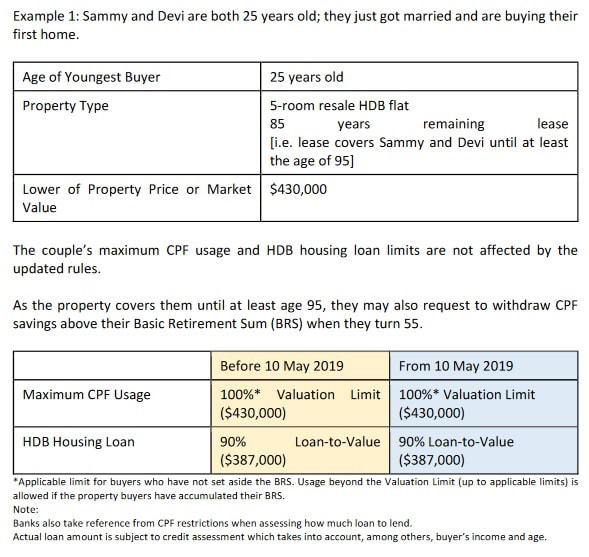

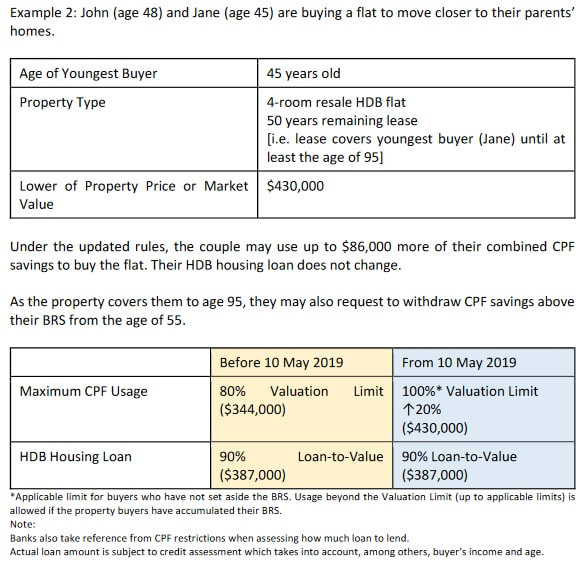

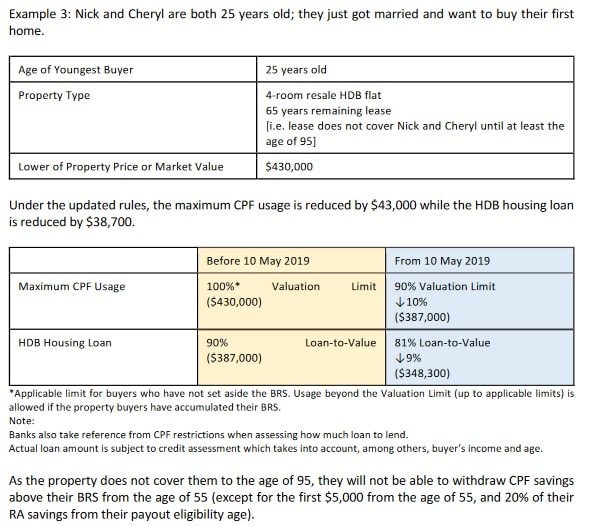

Examples:

Changes to purchase of multiple properties using CPF:

Previously, CPF members needed to set aside the Basic Retirement Sum (BRS) before excess Ordinary Account (OA) monies could be used to purchase second or subsequent properties.

From 10 May 2019, members who do not have any property bought using CPF monies that covers them until at least the age of 95 will need to set aside the Full Retirement Sum before using excess OA monies to purchase second or subsequent properties. Members who have a property with remaining lease that covers them until at least the age of 95 will not be affected (i.e. previous rules apply). Members in a buy-first-sell-later situation are not affected if they dispose of their previous property within the six-month grace period.

From 10 May 2019, members who do not have any property bought using CPF monies that covers them until at least the age of 95 will need to set aside the Full Retirement Sum before using excess OA monies to purchase second or subsequent properties. Members who have a property with remaining lease that covers them until at least the age of 95 will not be affected (i.e. previous rules apply). Members in a buy-first-sell-later situation are not affected if they dispose of their previous property within the six-month grace period.

Changes to CPF usage after age 55:

For purchases from 10 May 2019, the remaining lease of the property needs to cover the buyer until at least the age of 95 for the buyer to use Retirement Account (RA) savings above the BRS to pay for the property. Members approaching age 55 can ask CPF Board to reserve their OA savings so that they may continue servicing their mortgage payments after the age of 55. Those facing difficulty servicing their housing loans can approach HDB or CPF Board for assistance.

Find out how much CPF/Loan you can use for your property bought on or after 10 May 2019:

1. CPF (estimate) you can use => CPF Housing Calculator

2. HDB Loan (estimate) you can use => HDB Loan Estimate

2. HDB Loan (estimate) you can use => HDB Loan Estimate

Quick Reference guide for CPF/Loan: